Share This Post

Companies with strong and improving digital footprints, who engage their customers online, beat their rivals; that’s what the overwhelming evidence from the Digital Revenue Signal (DRS) has continued to show despite volatility across markets and strategies due to the coronavirus (see research notes from 2020 March and May) and fears of inflation.

DRS measures digital footprints at the brand and stock level using Web Traffic, Social Media, and Search Engine data, to predict the likely direction of revenue surprises and revenue growth. Companies with increases in attention are likely to experience increases in demand for their products and services, and therefore are likely to exceed the market’s expectations for revenues when they are announced.

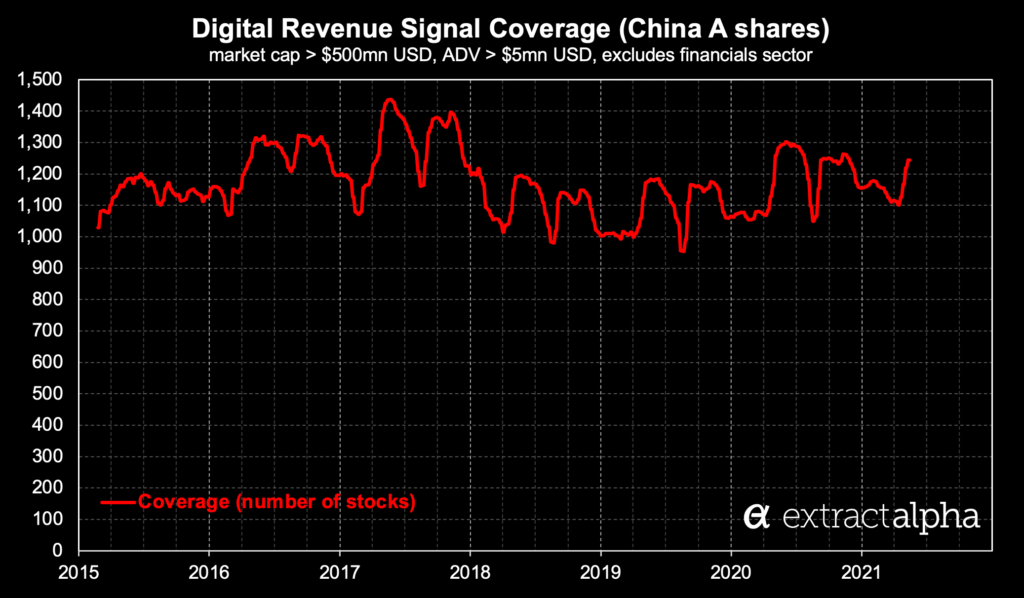

DRS currently covers 8,500+ stocks worldwide, including 1100+ China A shares and 500 HK stocks (includes H shares) since 20150223.

Delivery: daily data feed as csv before market open, 1-100 percentile score for likelihood of beating revenue estimates (with 4 subcomponents)

History: live since 20190901, in sample from 20150223

Contact us for free trial access to complete historical data

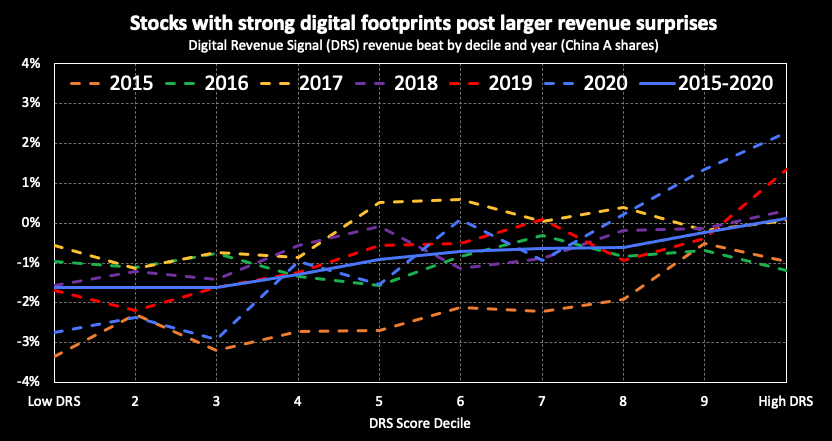

Using DRS each quarter, we track the percentage of companies that beat and miss their revenue estimates based on trends in online consumer engagement. We find that recent results were in line with both historical levels and with every year since DRS went live in 2019; low-ranked stocks miss and most high-ranked stocks beat their sell-side consensus revenue estimates, indicating that markets do not take into account this timely digital data which our clients have access to:

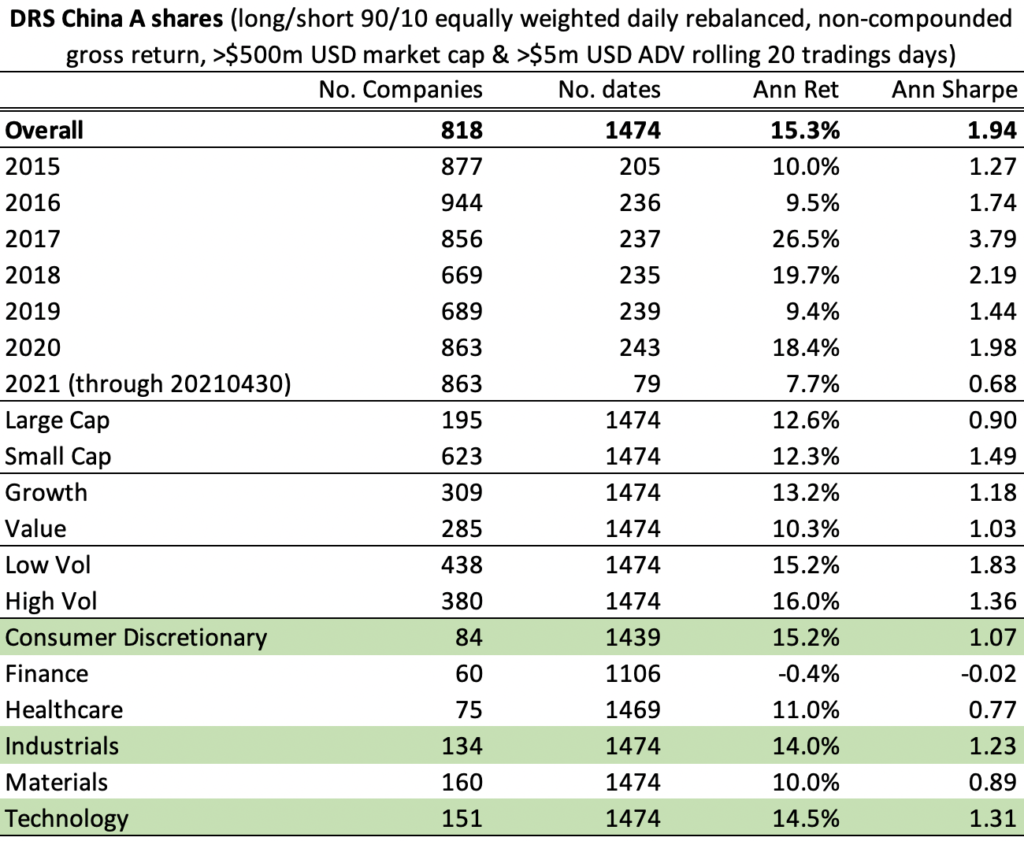

To demonstrate DRS as an alpha factor, our simple portfolio formed by going long the top-ranked decile of stocks and short the bottom decile (dollar neutral with no net exposure, daily rebalanced) delivered a robust +15.3% annualized non-compounded return and a Sharpe ratio of 1.94 before transaction costs (DRS would easily overcome transaction costs given the signal’s low turnover). A long-only top decile portfolio (100-130 stocks on average) delivered +22.9% annualized return and a Sharpe ratio of 0.70, a significant outperformance of more than double compared to its benchmark (CSI 800 index).

Simple cumulative returns, not compounded.

China A shares with market cap >= $500mm, ADV >= $5mm, excluding financial sector.

Equally weighted, rebalanced daily

Introduction Kentucky, famed for its bluegrass landscapes and bourbon heritage, is witnessing a quiet revolution in its financial sector with the rise of proprietary trading

Delving into the fascinating realm of behavioral finance, we encounter a field that seeks to understand the psychological factors influencing financial decision-making. From cognitive biases

Subscribe to the ExtractAlpha newsletter

© 2025 ExtractAlpha. All Rights Reserved.

Alan joined ExtractAlpha in 2024. He is a tenured associate professor of finance at the University of Hong Kong, where he serves as the program director of the MFFinTech, teaches classes on quantitative trading and big data in finance, and conducts research in finance specializing in big data and alternative datasets. He has published research in prestigious journals and regularly presents at financial conferences. He previously worked in technical and trading roles at DC Energy, Bridgewater Associates, Microsoft and advises several fintech startups. He received his PhD in finance from Cornell and his Bachelors from Dartmouth.

John joined ExtractAlpha in 2023 as the Director of Partnerships & Customer Success. He has extensive experience in the financial information services industry, having previously served as a Director of Client Specialist at Refinitiv. John holds dual Bachelor’s degrees in Commerce and Architecture (Design) from The University of Melbourne.

Matija is a specialist in software sales and customer success, bringing experience from various industries. His career, before sales, includes tech support, software development, and managerial roles. He earned his BSc and Specialist Degree in Electrical Engineering at the University of Montenegro.

Jack joined ExtractAlpha in 2022. Previously, he spent 20+ years supporting pre- and after-sales activities to drive sales in the Asia Pacific market. He has worked in many different industries including, technology, financial services, and manufacturing, where he developed excellent customer relationship management skills. He received his Bachelor of Business in Operations Management from the University of Technology Sydney.

Perry brings more than 20 years of Enterprise Software development, sales and customer engagement experience focused on Fortune 1000 customers. Prior to joining ExtractAlpha as a Technical Consultant, Perry was the founder, President and Chief Customer Officer at Solution Labs Inc. a data analytics company that specialized in the analysis of very large-scale computing infrastructures in place at some of the largest corporate data centers in the world.

Perry brings more than 20 years of Enterprise Software development, sales and customer engagement experience focused on Fortune 1000 customers. Prior to joining ExtractAlpha as a Technical Consultant, Perry was the founder, President and Chief Customer Officer at Solution Labs Inc. a data analytics company that specialized in the analysis of very large-scale computing infrastructures in place at some of the largest corporate data centers in the world.

Janette has 22+ years of leadership and management experience in FinTech and analytics sales and business development in the Asia Pacific region. In addition to expertise in quantitative models, she has worked on risk management, portfolio attribution, fund accounting, and custodian services. Janette is currently head of relationship management at Moody’s Analytics in the Asia-Pacific region, and was formerly Managing Director at State Street, head of sales for APAC Asset Management at Thomson Reuters, and head of Asia for StarMine. She is also a board member at Human Financial, a FinTech firm focused on the Australian superannuation industry.

Leigh founded Estimize in 2011. Prior to Estimize, Leigh ran Surfview Capital, a New York based quantitative investment management firm trading medium frequency momentum strategies. He was also an early member of the team at StockTwits where he worked on product and business development. Leigh is now the CEO of StarKiller Capital, an institutional investment management firm in the digital asset space.

Andrew is the CEO of Human Financial, a technology innovator that is pioneering consumer-led solutions for the superannuation industry. Andrew was previously CEO of Alpha Beta, a global quant hedge fund business. Prior to Alpha Beta he held senior roles in a number of hedge funds globally.

Jenny joined ExtractAlpha in 2023. Prior to that, she worked as a quantitative researcher for Chorus, a hedge fund under AXA Investment Managers. Jenny received her PhD in finance from the University of Hong Kong in 2023. Her research covers ESG, natural language processing, and market microstructure. Jenny received her Bachelor degree in Finance from The Chinese University of Hong Kong in 2019. Her research has been published in the Journal of Financial Markets.

Kristen joined ExtractAlpha in 2021 as a Sales Director. As a past employee of StarMine, Kristen has extensive experience in analyst performance analytics and helped to build out the sell-side solution, StarMine Monitor. She received her BS in Business Management from Cornell University.

Triloke has 10+ years experience in designing and developing software systems in the financial services industry. He joined ExtractAlpha in 2016. Prior to that, he worked as a senior software engineer at HSBC Global Technologies. He holds a Master of Applied Science degree from Ryerson University specializing in signal processing.

Qayyum (“Q”) joined ExtractAlpha in 2024 as the head of a new division, EA Labs. Q is a data scientist recognized for his innovative work in fintech and venture building. Prior to ExtractAlpha, he founded Nuu Ventures, a venture studio that acquired and scaled startups with a focus on lean growth and strategic exits. Previously, he co-founded iComply Investor Services and ESG Analytics, leveraging AI to assess ESG performance. A recipient of British Columbia’s Top 30 Under 30 award, Q also serves on the Fintech Advisory Committee for the BC Securities Commission and is known for his commitment to disrupting traditional business models through technology.

Yunan joined ExtractAlpha in 2019 as a quantitative researcher. Prior to that, he worked as a research analyst at ICBC, covering the macro economy and the Asian bond market. Yunan received his PhD in Economics & Finance from The University of Hong Kong in 2018. His research fields cover Empirical Asset Pricing, Mergers & Acquisitions, and Intellectual Property. His research outputs have been presented at major conferences such as AFA, FMA and FMA (Asia). Yunan received his Masters degree in Operations Research from London School of Economics in 2013 and his Bachelor degree in International Business from Nottingham University in 2012.

Prior to joining ExtractAlpha in 2022, Willett was a sales director for Vidrio Financial. Willett was based in Hong Kong for nearly two decades where he oversaw FIS Global’s Asset Management and Commercial Banking efforts. Willett worked at FactSet, where he built the Asian Portfolio and Quantitative Analytics team and oversaw FactSet’s Southeast Asian operations. Willett completed his undergraduate studies at Georgetown University and finished a joint degree MBA from the Northwestern Kellogg School and the Hong Kong University of Science and Technology in 2010. Willett also holds the Chartered Financial Analyst (CFA) designation.

Julie Craig is a senior marketing executive with decades of experience marketing high tech, fintech, and financial services offerings. She joined ExtractAlpha in 2022. She was formerly with AlphaSense, where she led marketing at a startup now valued at $4B. Prior to that, she was with Interactive Data where she led marketing initiatives and a multi-million dollar budget for an award-winning product line for individual and institutional investors.

Jeff is the CFO and COO of ExtractAlpha and directs our financial, strategic, and general management operations. He previously held the role of CFO at Estimize and two publicly traded firms, Multex and Market Guide. Jeff also served as CFO at private-equity backed companies, including Coleman Research, Ford Models, Instant Information, and Moneyline Telerate. He’s also held roles as advisor, partner, and board member at Total Reliance, CreditRiskMonitor, Mochidoki, and Resurge.

Vinesh founded ExtractAlpha in 2013 with the mission of bringing analytical rigor to the analysis and marketing of new datasets for the capital markets. Since ExtractAlpha’s merger with Estimize in early 2021, he has served as the CEO of both entities. From 1999 to 2005, Vinesh was the Director of Quantitative Research at StarMine in San Francisco, where he developed industry leading metrics of sell side analyst performance as well as successful commercial alpha signals and products based on analyst, fundamental, and other data sources. Subsequently, he developed systematic trading strategies for proprietary trading desks at Merrill Lynch and Morgan Stanley in New York. Most recently he was Executive Director at PDT Partners, a spinoff of Morgan Stanley’s premiere quant prop trading group, where in addition to research, he also applied his experience in the communication of complex quantitative concepts to investor relations. Vinesh holds an undergraduate degree from the University of Chicago and a graduate degree from the University of Cambridge, both in mathematics.